Bankruptcy Prediction Tutorial

0. Overview

As part of a collaboration, teams from Crédit Agricole CIB and Quandela have developed a hybrid classical-quantum model to classify fallen angels from a credit scoring dataset. In simple terms, a fallen angel is a bond that used to be safe, but that is now risky (its quality decreased). However, the dataset used in the original project is private, so we will instead work, in this notebook, with an open-source dataset on company bankruptcy prediction. This task is similar to fallen angel classification in many ways:

Modelization of a regime change (from healty to unhealthy)

Time dependent

Goal of detecting early warning signs

Imbalanced dataset (bankruptcy and fallen angels are rarer than their counterpart)

Similar feature space that relies on economic metrics

The specific dataset we use is a bankruptcy dataset from the Taiwan Economic Journal (1999-2009). A notebook on prediction for this dataset is also presented, which helped with the construction of this current notebook.

1. Imports

All imports and handdling of random seeds.

[ ]:

import matplotlib.pyplot as plt

import merlin as ML

import numpy as np

import os

import pandas as pd

import random

import torch

from imblearn.over_sampling import RandomOverSampler

from scipy.optimize import minimize

from scipy.special import expit

from sklearn.base import BaseEstimator, ClassifierMixin

from sklearn.decomposition import PCA

from sklearn.ensemble import AdaBoostClassifier

from sklearn.metrics import auc, precision_recall_curve, roc_curve

from sklearn.model_selection import train_test_split

from sklearn.neighbors import KNeighborsClassifier

from sklearn.preprocessing import StandardScaler

from sklearn.tree import DecisionTreeClassifier

from tqdm.auto import tqdm

# Deterministic setup

SEED = 42

os.environ["PYTHONHASHSEED"] = str(SEED)

random.seed(SEED)

np.random.seed(SEED)

torch.manual_seed(SEED)

<torch._C.Generator at 0x12876d930>

2. Dataset

We will fetch the bankruptcy prediction dataset from Kaggle, an online platform to share datasets, build and run machine learning models, and compete in data science challenges. To access the data, you need to have (or will need to create) an access token on Kaggle. Here are the simple steps to create your access token:

Go to the Kaggle website

Register or sign in if you already have an account

Once that is done, click on your profile image in the top right corner

Select account

Scroll to the API section and click on “Create New Token”

This should trigger a download of a file called kaggle.json containing your username and API key.

In this file, copy your API key and set it as a variable in the next cell

[ ]:

KAGGLE_API_TOKEN = "{YOUR_KAGGLE_API_TOKEN}"

Next we install kaggle.

[3]:

!pip install kaggle

Requirement already satisfied: kaggle in ./.venv/lib/python3.13/site-packages (2.0.0)

Requirement already satisfied: bleach in ./.venv/lib/python3.13/site-packages (from kaggle) (6.3.0)

Requirement already satisfied: kagglesdk<1.0,>=0.1.15 in ./.venv/lib/python3.13/site-packages (from kaggle) (0.1.16)

Requirement already satisfied: packaging in ./.venv/lib/python3.13/site-packages (from kaggle) (26.0)

Requirement already satisfied: protobuf in ./.venv/lib/python3.13/site-packages (from kaggle) (7.34.1)

Requirement already satisfied: python-dateutil in ./.venv/lib/python3.13/site-packages (from kaggle) (2.9.0.post0)

Requirement already satisfied: python-slugify in ./.venv/lib/python3.13/site-packages (from kaggle) (8.0.4)

Requirement already satisfied: requests in ./.venv/lib/python3.13/site-packages (from kaggle) (2.33.1)

Requirement already satisfied: tqdm in ./.venv/lib/python3.13/site-packages (from kaggle) (4.67.3)

Requirement already satisfied: urllib3>=1.15.1 in ./.venv/lib/python3.13/site-packages (from kaggle) (2.6.3)

Requirement already satisfied: webencodings in ./.venv/lib/python3.13/site-packages (from bleach->kaggle) (0.5.1)

Requirement already satisfied: six>=1.5 in ./.venv/lib/python3.13/site-packages (from python-dateutil->kaggle) (1.17.0)

Requirement already satisfied: text-unidecode>=1.3 in ./.venv/lib/python3.13/site-packages (from python-slugify->kaggle) (1.3)

Requirement already satisfied: charset_normalizer<4,>=2 in ./.venv/lib/python3.13/site-packages (from requests->kaggle) (3.4.6)

Requirement already satisfied: idna<4,>=2.5 in ./.venv/lib/python3.13/site-packages (from requests->kaggle) (3.11)

Requirement already satisfied: certifi>=2023.5.7 in ./.venv/lib/python3.13/site-packages (from requests->kaggle) (2026.2.25)

[notice] A new release of pip is available: 25.1.1 -> 26.0.1

[notice] To update, run: pip install --upgrade pip

We can now access the dataset and download it locally. This cell should download a zip file called american-companies-bankruptcy-prediction-dataset.zip.

[4]:

!kaggle datasets download -d fedesoriano/company-bankruptcy-prediction

Dataset URL: https://www.kaggle.com/datasets/fedesoriano/company-bankruptcy-prediction

License(s): copyright-authors

Downloading company-bankruptcy-prediction.zip to /Users/philippeschoeb/Documents/fallen_angels_project/ensemble-quantum-classifier

100%|██████████████████████████████████████| 4.63M/4.63M [00:01<00:00, 4.73MB/s]

We unzip this file to obtain the dataset.

[5]:

!unzip company-bankruptcy-prediction.zip

Archive: company-bankruptcy-prediction.zip

inflating: data.csv

We finally have our dataset locally. We now need to preprocess it before moving on to the model implementation.

[241]:

df = pd.read_csv("./data.csv")

df.head()

[241]:

| Bankrupt? | ROA(C) before interest and depreciation before interest | ROA(A) before interest and % after tax | ROA(B) before interest and depreciation after tax | Operating Gross Margin | Realized Sales Gross Margin | Operating Profit Rate | Pre-tax net Interest Rate | After-tax net Interest Rate | Non-industry income and expenditure/revenue | ... | Net Income to Total Assets | Total assets to GNP price | No-credit Interval | Gross Profit to Sales | Net Income to Stockholder's Equity | Liability to Equity | Degree of Financial Leverage (DFL) | Interest Coverage Ratio (Interest expense to EBIT) | Net Income Flag | Equity to Liability | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.370594 | 0.424389 | 0.405750 | 0.601457 | 0.601457 | 0.998969 | 0.796887 | 0.808809 | 0.302646 | ... | 0.716845 | 0.009219 | 0.622879 | 0.601453 | 0.827890 | 0.290202 | 0.026601 | 0.564050 | 1 | 0.016469 |

| 1 | 1 | 0.464291 | 0.538214 | 0.516730 | 0.610235 | 0.610235 | 0.998946 | 0.797380 | 0.809301 | 0.303556 | ... | 0.795297 | 0.008323 | 0.623652 | 0.610237 | 0.839969 | 0.283846 | 0.264577 | 0.570175 | 1 | 0.020794 |

| 2 | 1 | 0.426071 | 0.499019 | 0.472295 | 0.601450 | 0.601364 | 0.998857 | 0.796403 | 0.808388 | 0.302035 | ... | 0.774670 | 0.040003 | 0.623841 | 0.601449 | 0.836774 | 0.290189 | 0.026555 | 0.563706 | 1 | 0.016474 |

| 3 | 1 | 0.399844 | 0.451265 | 0.457733 | 0.583541 | 0.583541 | 0.998700 | 0.796967 | 0.808966 | 0.303350 | ... | 0.739555 | 0.003252 | 0.622929 | 0.583538 | 0.834697 | 0.281721 | 0.026697 | 0.564663 | 1 | 0.023982 |

| 4 | 1 | 0.465022 | 0.538432 | 0.522298 | 0.598783 | 0.598783 | 0.998973 | 0.797366 | 0.809304 | 0.303475 | ... | 0.795016 | 0.003878 | 0.623521 | 0.598782 | 0.839973 | 0.278514 | 0.024752 | 0.575617 | 1 | 0.035490 |

5 rows × 96 columns

Exploration of the dataset:

[242]:

df.info()

<class 'pandas.DataFrame'>

RangeIndex: 6819 entries, 0 to 6818

Data columns (total 96 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Bankrupt? 6819 non-null int64

1 ROA(C) before interest and depreciation before interest 6819 non-null float64

2 ROA(A) before interest and % after tax 6819 non-null float64

3 ROA(B) before interest and depreciation after tax 6819 non-null float64

4 Operating Gross Margin 6819 non-null float64

5 Realized Sales Gross Margin 6819 non-null float64

6 Operating Profit Rate 6819 non-null float64

7 Pre-tax net Interest Rate 6819 non-null float64

8 After-tax net Interest Rate 6819 non-null float64

9 Non-industry income and expenditure/revenue 6819 non-null float64

10 Continuous interest rate (after tax) 6819 non-null float64

11 Operating Expense Rate 6819 non-null float64

12 Research and development expense rate 6819 non-null float64

13 Cash flow rate 6819 non-null float64

14 Interest-bearing debt interest rate 6819 non-null float64

15 Tax rate (A) 6819 non-null float64

16 Net Value Per Share (B) 6819 non-null float64

17 Net Value Per Share (A) 6819 non-null float64

18 Net Value Per Share (C) 6819 non-null float64

19 Persistent EPS in the Last Four Seasons 6819 non-null float64

20 Cash Flow Per Share 6819 non-null float64

21 Revenue Per Share (Yuan ¥) 6819 non-null float64

22 Operating Profit Per Share (Yuan ¥) 6819 non-null float64

23 Per Share Net profit before tax (Yuan ¥) 6819 non-null float64

24 Realized Sales Gross Profit Growth Rate 6819 non-null float64

25 Operating Profit Growth Rate 6819 non-null float64

26 After-tax Net Profit Growth Rate 6819 non-null float64

27 Regular Net Profit Growth Rate 6819 non-null float64

28 Continuous Net Profit Growth Rate 6819 non-null float64

29 Total Asset Growth Rate 6819 non-null float64

30 Net Value Growth Rate 6819 non-null float64

31 Total Asset Return Growth Rate Ratio 6819 non-null float64

32 Cash Reinvestment % 6819 non-null float64

33 Current Ratio 6819 non-null float64

34 Quick Ratio 6819 non-null float64

35 Interest Expense Ratio 6819 non-null float64

36 Total debt/Total net worth 6819 non-null float64

37 Debt ratio % 6819 non-null float64

38 Net worth/Assets 6819 non-null float64

39 Long-term fund suitability ratio (A) 6819 non-null float64

40 Borrowing dependency 6819 non-null float64

41 Contingent liabilities/Net worth 6819 non-null float64

42 Operating profit/Paid-in capital 6819 non-null float64

43 Net profit before tax/Paid-in capital 6819 non-null float64

44 Inventory and accounts receivable/Net value 6819 non-null float64

45 Total Asset Turnover 6819 non-null float64

46 Accounts Receivable Turnover 6819 non-null float64

47 Average Collection Days 6819 non-null float64

48 Inventory Turnover Rate (times) 6819 non-null float64

49 Fixed Assets Turnover Frequency 6819 non-null float64

50 Net Worth Turnover Rate (times) 6819 non-null float64

51 Revenue per person 6819 non-null float64

52 Operating profit per person 6819 non-null float64

53 Allocation rate per person 6819 non-null float64

54 Working Capital to Total Assets 6819 non-null float64

55 Quick Assets/Total Assets 6819 non-null float64

56 Current Assets/Total Assets 6819 non-null float64

57 Cash/Total Assets 6819 non-null float64

58 Quick Assets/Current Liability 6819 non-null float64

59 Cash/Current Liability 6819 non-null float64

60 Current Liability to Assets 6819 non-null float64

61 Operating Funds to Liability 6819 non-null float64

62 Inventory/Working Capital 6819 non-null float64

63 Inventory/Current Liability 6819 non-null float64

64 Current Liabilities/Liability 6819 non-null float64

65 Working Capital/Equity 6819 non-null float64

66 Current Liabilities/Equity 6819 non-null float64

67 Long-term Liability to Current Assets 6819 non-null float64

68 Retained Earnings to Total Assets 6819 non-null float64

69 Total income/Total expense 6819 non-null float64

70 Total expense/Assets 6819 non-null float64

71 Current Asset Turnover Rate 6819 non-null float64

72 Quick Asset Turnover Rate 6819 non-null float64

73 Working capitcal Turnover Rate 6819 non-null float64

74 Cash Turnover Rate 6819 non-null float64

75 Cash Flow to Sales 6819 non-null float64

76 Fixed Assets to Assets 6819 non-null float64

77 Current Liability to Liability 6819 non-null float64

78 Current Liability to Equity 6819 non-null float64

79 Equity to Long-term Liability 6819 non-null float64

80 Cash Flow to Total Assets 6819 non-null float64

81 Cash Flow to Liability 6819 non-null float64

82 CFO to Assets 6819 non-null float64

83 Cash Flow to Equity 6819 non-null float64

84 Current Liability to Current Assets 6819 non-null float64

85 Liability-Assets Flag 6819 non-null int64

86 Net Income to Total Assets 6819 non-null float64

87 Total assets to GNP price 6819 non-null float64

88 No-credit Interval 6819 non-null float64

89 Gross Profit to Sales 6819 non-null float64

90 Net Income to Stockholder's Equity 6819 non-null float64

91 Liability to Equity 6819 non-null float64

92 Degree of Financial Leverage (DFL) 6819 non-null float64

93 Interest Coverage Ratio (Interest expense to EBIT) 6819 non-null float64

94 Net Income Flag 6819 non-null int64

95 Equity to Liability 6819 non-null float64

dtypes: float64(93), int64(3)

memory usage: 5.0 MB

We look at the number of missing data.

[243]:

(df.isna().sum() > 0).sum()

[243]:

np.int64(0)

So no data is missing.

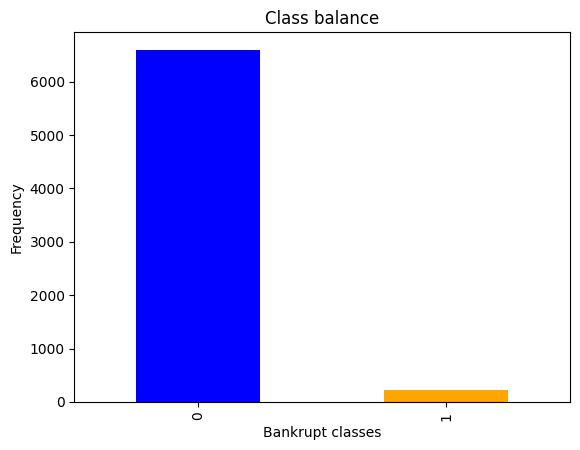

Next, we look at the count for each label (0: healthy, 1: bankrupt).

[244]:

df["Bankrupt?"].value_counts().plot(kind="bar", color=["blue", "orange"])

plt.xlabel("Bankrupt classes")

plt.ylabel("Frequency")

plt.title("Class balance")

print(df["Bankrupt?"].value_counts(normalize=True))

Bankrupt?

0 0.967737

1 0.032263

Name: proportion, dtype: float64

2.1 Dataset Splits

Now, we separate the dataset into three sets: the train, validation and the test sets.

[245]:

target = "Bankrupt?"

X = df.drop(columns=[target])

y = df[target]

print(f"Before splitting: {X.shape}, {y.shape}")

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.3, random_state=42

)

print(f"X_train shape: {X_train.shape}, y_train shape: {y_train.shape}")

# We then split test set into validation and test sets

X_val, X_test, y_val, y_test = train_test_split(

X_test, y_test, test_size=0.5, random_state=42

)

print(f"X_val shape: {X_val.shape}, y_val shape: {y_val.shape}")

print(f"X_test shape: {X_test.shape}, y_test shape: {y_test.shape}")

Before splitting: (6819, 95), (6819,)

X_train shape: (4773, 95), y_train shape: (4773,)

X_val shape: (1023, 95), y_val shape: (1023,)

X_test shape: (1023, 95), y_test shape: (1023,)

2.2 Oversampling

We apply oversampling to reduce the effect of the dataset labels imbalancement during training.

[246]:

ros = RandomOverSampler(random_state=42)

X_train, y_train = ros.fit_resample(X_train, y_train)

print(f"After resampling: {X_train.shape}, {y_train.shape}")

print(

f"Class distribution after resampling:\n{pd.Series(y_train).value_counts(normalize=True)}"

)

After resampling: (9262, 95), (9262,)

Class distribution after resampling:

Bankrupt?

0 0.5

1 0.5

Name: proportion, dtype: float64

2.3 Standardization

Next, we want to standardize our data as preprocessing. That is to induce mean = 0 and variance = 1 to every feature of the training set (and applying the same transformation to the validation and test sets).

[247]:

scaler = StandardScaler()

X_train = scaler.fit_transform(X_train)

X_val = scaler.transform(X_val)

X_test = scaler.transform(X_test)

X_train.mean(axis=0), X_train.std(axis=0)

[247]:

(array([ 1.96392723e-16, -6.87374532e-16, -7.85570893e-16, 2.92134176e-15,

-3.16683266e-15, -2.22491475e-14, -2.72494904e-15, -4.31757128e-15,

4.43724809e-15, 1.51590633e-15, -1.53431815e-17, -9.20590891e-17,

-2.08667269e-15, 0.00000000e+00, -1.22745452e-16, 9.81963617e-17,

-4.41883628e-16, -2.45490904e-16, 0.00000000e+00, 8.10119984e-16,

-6.13727260e-18, -2.45490904e-16, 4.41883628e-16, -8.13188620e-17,

-1.00774016e-14, 3.35708811e-15, 4.90981808e-15, 2.12656496e-15,

2.45490904e-17, -1.53431815e-18, -2.22476132e-15, 8.34669074e-16,

1.22745452e-17, 0.00000000e+00, 4.07284753e-15, -1.22745452e-17,

-9.81963617e-17, 2.94589085e-16, 5.52354534e-17, -8.59218165e-17,

9.20590891e-17, 1.71843633e-16, 1.96392723e-16, -3.68236356e-16,

1.22745452e-17, -7.47980099e-18, -1.53431815e-18, -1.01264998e-16,

4.90981808e-17, 4.29609082e-17, -6.13727260e-18, 6.62825441e-16,

-3.06863630e-18, -1.47294543e-16, -1.47294543e-16, 7.36472713e-17,

0.00000000e+00, 1.53431815e-18, 0.00000000e+00, 4.90981808e-17,

3.80510901e-16, -1.38779077e-15, 1.53431815e-18, 3.11274795e-16,

-2.23396723e-15, 2.94589085e-16, 1.07402271e-17, -1.47294543e-16,

-7.11923622e-16, -2.20941814e-16, 4.52623855e-17, 1.22745452e-16,

5.90443982e-15, 4.90981808e-17, 2.33983518e-15, 4.90981808e-17,

3.11274795e-16, 2.94589085e-16, 9.81963617e-17, 2.94589085e-16,

1.32565088e-15, -3.19138175e-16, -1.77980906e-15, -9.81963617e-17,

0.00000000e+00, 8.83767255e-16, 0.00000000e+00, -8.15336665e-15,

1.93937814e-15, 1.04333634e-15, -9.20590891e-16, 1.31184202e-16,

1.23926877e-14, 0.00000000e+00, -2.45490904e-17]),

array([1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1.,

1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1.,

1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1.,

1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1.,

1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1., 1.,

1., 1., 1., 1., 1., 1., 1., 1., 0., 1.]))

2.4 Build The Dataset

Now that our original features are preprocessed, we will use Principle Component Analysis to only consider 5 features instead of 18 to mimic the original fallen angel prediction framework which presented 5 features.

[248]:

pca = PCA(n_components=5)

X_train_pca = pca.fit_transform(X_train)

X_val_pca = pca.transform(X_val)

X_test_pca = pca.transform(X_test)

X_train_pca.shape, X_val_pca.shape, X_test_pca.shape

[248]:

((9262, 5), (1023, 5), (1023, 5))

[249]:

pca.explained_variance_ratio_

[249]:

array([0.16948571, 0.07214918, 0.0653974 , 0.05641544, 0.04374511])

Since there are 95 features, it is normal to lose a big part of the original dataset variance by using PCA to reduce dimentionality to 5.

2.5 Angle Encoding

In the original implementation, quantum models use an angle-like preprocessing before before entering photonic circuits through angle encoding. Each feature is transformed with a sigmoid rescaling into [0, pi], using train-set statistics.

We apply this preprocessing to the dataset now, for later use in the hybrid model.

[250]:

def transform_features_to_phases(x, means=None, stds=None):

"""Feature-to-phase transform: pi / (1 + exp(-(x-mean)/std))."""

x = np.asarray(x, dtype=np.float32)

if means is None:

means = x.mean(axis=0)

if stds is None:

stds = x.std(axis=0)

stds = np.where(stds < 1e-12, 1.0, stds)

z = (x - means) / stds

# phases = np.pi / (1.0 + np.exp(-z))

phases = np.pi * expit(z) # more stable version

return phases, means, stds

X_train_pca_angle, pca_angle_means, pca_angle_stds = transform_features_to_phases(

X_train_pca

)

X_val_pca_angle, _, _ = transform_features_to_phases(

X_val_pca, pca_angle_means, pca_angle_stds

)

X_test_pca_angle, _, _ = transform_features_to_phases(

X_test_pca, pca_angle_means, pca_angle_stds

)

3. Model Definitions

We define two models:

Classical AdaBoost (baseline).

Quantum-Enhanced AdaBoost which comprises of several branches:

The first branch send the input through the classical AdaBoost model

The remaining branches send the input through k different Quantum Classifiers Afterward, the final score is an optimized weighted sum of the obtained scores from every branch.

The quantum classifiers are made of fixed (non-trainable) quantum circuits followed by a trainable linear readout.

[251]:

class ClassicalAdaBoost:

def __init__(self, n_estimators=50, max_depth=3, random_state=42):

base_tree = DecisionTreeClassifier(

max_depth=max_depth, random_state=random_state

)

self.model = AdaBoostClassifier(

estimator=base_tree,

n_estimators=n_estimators,

random_state=10,

)

def fit(self, x_train, y_train):

self.model.fit(x_train, y_train)

def predict(self, x):

return self.model.predict(x)

def predict_proba(self, x):

return self.model.predict_proba(x)[:, 1]

Next we define the quantum classifier model class:

[252]:

class QuantumClassifier(torch.nn.Module):

"""

A simple quantum classifier model that consists of a trainable quantum layer followed by a trainable linear readout.

"""

def __init__(self, n_features=5):

super().__init__()

self.n_features = n_features

self.quantum_layer = self.create_quantum_layer()

self.readout = torch.nn.Linear(self.quantum_layer.output_size, 1)

self.readout

def create_quantum_layer(self):

builder = ML.CircuitBuilder(n_modes=self.n_features)

# Start by placing an entangling layer

builder.add_entangling_layer(modes=[0, self.n_features - 1], trainable=True)

# Encode the data using angle encoding on all modes

builder.add_angle_encoding(modes=list(range(self.n_features)), name="data")

# Add another entangling layer after the encoding

builder.add_entangling_layer(modes=[0, self.n_features - 1], trainable=True)

# Define quantum layer

quantum_layer = ML.QuantumLayer(

builder=builder,

input_state=[1, 0, 1, 0, 0],

measurement_strategy=ML.MeasurementStrategy.probs(

computation_space=ML.ComputationSpace.FOCK

),

)

return quantum_layer

def forward(self, x):

"""

It is assumed here that the input x is already "angle transformed"

"""

assert len(x.shape) == 2, (

"Input must be a 2D tensor of shape (n_samples, n_features)"

)

n_sample = x.shape[0]

n_features = x.shape[1]

assert n_features == self.n_features, (

f"Expected {self.n_features} features, got {n_features}"

)

# Assume x is already in angle-encoded form

q_out = self.quantum_layer(x)

q_score = torch.sigmoid(self.readout(q_out))

assert q_score.shape == (n_sample, 1), (

f"Expected output shape (n_samples, 1), got {q_score.shape}"

)

return q_score.squeeze()

[253]:

# Check that the number of parameters fits the expected number for the defined quantum layer and readout

qc = QuantumClassifier(n_features=5)

total_params = sum(p.numel() for p in qc.parameters())

print(f"Total parameters in QuantumClassifier: {total_params}")

circuit_params = sum(p.numel() for p in qc.quantum_layer.parameters())

expected_params = (

circuit_params + qc.quantum_layer.output_size + 1

) # circuit params +readout weights + bias

print(

f"Expected parameters (circuit params + readout weights + bias): {expected_params}"

)

assert total_params == expected_params, (

f"Expected {expected_params} parameters, but got {total_params}"

)

Total parameters in QuantumClassifier: 56

Expected parameters (circuit params + readout weights + bias): 56

Next we move on to the more general QuantumEnhancedAdaBoost model.

It expects at initialization an already fitted classical AdaBoost model and already trained quantum_estimators.

Some methods for optimization of the ensembling weights are then defined precision_at_fixed_recall and optimize_nonnegative_weights. These methods are used in the fit method which encapsulates all the training for this weight vector. Because the dataset we use here is highly unbalanced, the metric of interest is the precision at a fixed recall of 83%. We can interpet this as:

The model correctly identifies 83% of the actual bankruptcy

Measure precision: among the bankruptcy predictions, how many are correct?

The weight vector (which combines outputs from every submodel) is optimized with regard to this metric.

[254]:

def precision_at_fixed_recall(y_true, y_scores, target_recall=0.83):

"""

Get maximum precision at recall >= target_recall.

If no recall value is above target_recall, return NaN.

"""

precision, recall, _ = precision_recall_curve(y_true, y_scores)

mask = recall >= target_recall

if not np.any(mask):

return np.nan

return float(np.max(precision[mask]))

In the hybrid model (QuantumEnhancedAdaBoost), we enforce two constraints on the unifying weights:

The sum of the weigth vector must equal 1 to ensure a fusion of scores that does not scale.

Each weight value must be positive to ensure every submodel is used as intended for the final prediction.

The final optimized value of the weights must be superior to their initial value divised by the number of submodels. That is to ensure no submodel is completelly ignored while giving the complete hybrid model a margin that scales with the number of submodels to choose which submodel to consider with more importance.

[255]:

class QuantumEnhancedAdaBoost(BaseEstimator, ClassifierMixin):

def __init__(self, classical_model, quantum_estimators):

"""

Initializes the QuantumEnhancedAdaBoost model.

Args:

classical_model: The fitted classical AdaBoost model.

quantum_estimators: A list of already trained quantum estimators to be used.

"""

self.classical_model = classical_model

self.quantum_estimators = quantum_estimators

self.n_quantum = len(quantum_estimators)

self.weights = np.ones(self.n_quantum + 1) / (

self.n_quantum + 1

) # Initialize weights equally

def optimize_nonnegative_weights(self, scores, y_true, target_recall=0.83):

"""

Optimize non-negative ensemble weights to maximize precision at fixed recall,

while enforcing a minimum per-component contribution.

scores shape: (n_components, n_samples)

"""

n_components = scores.shape[0]

init = self.weights.copy()

# Constraint: each weight >= initial_value / n_components.

# With equal initialization, initial_value = 1 / n_components, so min_weight = 1 / n_components^2.

initial_value = float(init[0])

min_weight = initial_value / n_components

# Keep a small safety margin from exact bounds for numerical stability.

eps = 1e-12

min_weight = max(0.0, min(min_weight, 1.0 / n_components - eps))

def objective(w):

combined_scores = w @ scores

precision = precision_at_fixed_recall(

y_true, combined_scores, target_recall=target_recall

)

if np.isnan(precision):

return 1e6

return -precision

# Feasible initialization inside simplex with lower-bounded components.

init = np.clip(init, min_weight, None)

init = init / init.sum()

if np.any(init < min_weight):

# If clipping + normalization drifts below bound, rebuild from slack allocation.

slack = 1.0 - n_components * min_weight

if slack <= 0:

init = np.ones(n_components) / n_components

else:

extra = np.maximum(self.weights - self.weights.min(), 0.0)

if extra.sum() == 0:

extra = np.ones(n_components)

extra = extra / extra.sum()

init = min_weight + slack * extra

# COBYLA supports inequality constraints only.

# Enforce sum(w)=1 with two inequalities using a small tolerance.

eq_tol = 1e-9

constraints = [

{"type": "ineq", "fun": lambda w: w - min_weight},

{"type": "ineq", "fun": lambda w: np.sum(w) - (1.0 - eq_tol)},

{"type": "ineq", "fun": lambda w: (1.0 + eq_tol) - np.sum(w)},

]

result = minimize(

objective,

x0=init,

method="COBYLA",

constraints=constraints,

options={"maxiter": 2000, "tol": 1e-9, "catol": 1e-9},

)

if result.success:

weights = result.x

else:

weights = init

# Final projection for robustness against tiny numerical violations.

weights = np.clip(weights, min_weight, None)

weights = weights / weights.sum()

self.weights = weights

return

def fit(self, X, X_angle, y):

classical_score = self.classical_model.predict_proba(X)

quantum_scores = [

quantum_estimator(torch.tensor(X_angle, dtype=torch.float32))

.detach()

.numpy()

for quantum_estimator in self.quantum_estimators

]

scores = np.vstack([classical_score] + quantum_scores)

assert scores.shape == (self.n_quantum + 1, X.shape[0]), (

f"Expected scores shape ({self.n_quantum + 1}, n_samples), got {scores.shape}"

)

self.optimize_nonnegative_weights(scores, y)

def predict(self, X, X_angle):

classical_score = self.classical_model.predict_proba(X)

quantum_scores = [

quantum_estimator(torch.tensor(X_angle, dtype=torch.float32))

.detach()

.numpy()

for quantum_estimator in self.quantum_estimators

]

scores = np.vstack([classical_score] + quantum_scores)

assert scores.shape == (self.n_quantum + 1, X.shape[0]), (

f"Expected scores shape ({self.n_quantum + 1}, n_samples), got {scores.shape}"

)

combined_scores = self.weights @ scores

return (combined_scores >= 0.5).astype(float)

def predict_proba(self, X, X_angle):

classical_score = self.classical_model.predict_proba(X)

quantum_scores = [

quantum_estimator(torch.tensor(X_angle, dtype=torch.float32))

.detach()

.numpy()

for quantum_estimator in self.quantum_estimators

]

scores = np.vstack([classical_score] + quantum_scores)

assert scores.shape == (self.n_quantum + 1, X.shape[0]), (

f"Expected scores shape ({self.n_quantum + 1}, n_samples), got {scores.shape}"

)

combined_scores = self.weights @ scores

return combined_scores

4. Baseline Models

4.1 Neural Network

Let us also define a classical Neural Network baseline.

[256]:

class NeuralNetWork(torch.nn.Module):

def __init__(self, n_features=5, hidden_size=4):

super().__init__()

self.model = torch.nn.Sequential(

torch.nn.Linear(n_features, hidden_size),

torch.nn.ReLU(),

torch.nn.Linear(hidden_size, 1),

torch.nn.Sigmoid(),

)

def forward(self, x):

return self.model(x).squeeze()

4.2 K-NN

We define a k-nearest-neighbours classifier.

[257]:

knn_pca = KNeighborsClassifier(n_neighbors=5)

5. Training

The training will be done in several steps.

Train the classical AdaBoost model (on the training set)

[258]:

adaboost_pca = ClassicalAdaBoost()

print("Fitting classical AdaBoost model on PCA dataset...")

adaboost_pca.fit(X_train_pca, y_train)

Fitting classical AdaBoost model on PCA dataset...

We define a function to analyze performance of an sklearn model on the train set and a test set.

[259]:

def sklearn_model_analysis(model, X_train, y_train, X_test, y_test):

train_preds = model.predict(X_train)

test_preds = model.predict(X_test)

train_probas = model.predict_proba(X_train)

test_probas = model.predict_proba(X_test)

# Handle binary classification case where predict_proba returns shape (n_samples, 2)

if train_probas.ndim > 1 and train_probas.shape[1] > 1:

train_probas = train_probas[:, 1]

if test_probas.ndim > 1 and test_probas.shape[1] > 1:

test_probas = test_probas[:, 1]

train_precision = precision_at_fixed_recall(

y_train, train_probas, target_recall=0.83

)

test_precision = precision_at_fixed_recall(y_test, test_probas, target_recall=0.83)

print(f"MODEL OUTPUT ANALYSIS:#####################################")

print(

f"Number of positive predictions (class 1.0) on train set: {(train_preds == 1.0).sum()} out of {len(train_preds)}"

)

print(

f"Number of positive predictions (class 1.0) on test set: {(test_preds == 1.0).sum()} out of {len(test_preds)}"

)

print(f"\nTRAIN METRICS:#####################################")

print(

f"Accuracy: {(train_preds == y_train).mean():.4f}, Precision at 83% recall: {train_precision:.4f}"

)

print(f"\nTEST METRICS:#####################################")

print(

f"Accuracy: {(test_preds == y_test).mean():.4f}, Precision at 83% recall: {test_precision:.4f}"

)

only_zero = np.array([0.0] * len(y_test))

only_one = np.array([1.0] * len(y_test))

random_outputs = np.random.rand(len(y_test))

random_preds = (random_outputs >= 0.5).astype(float)

accuracy_only_zero = np.mean(only_zero == y_test)

accuracy_only_one = np.mean(only_one == y_test)

accuracy_random = np.mean(random_preds == y_test)

precision_random = precision_at_fixed_recall(

y_test, random_outputs, target_recall=0.83

)

print(f"\nTRIVIAL BASELINE TEST METRICS:#####################################")

print(f"Test accuracy (only zeros): {accuracy_only_zero:.4f}")

print(f"Test accuracy (only ones): {accuracy_only_one:.4f}")

print(

f"Test accuracy (random): {accuracy_random:.4f}, Precision at 83% recall (random) on test: {precision_random:.4f}"

)

5.1 AdaBoost Output And Performance Analysis (Train And Validation)

[260]:

sklearn_model_analysis(adaboost_pca, X_train_pca, y_train, X_val_pca, y_val)

MODEL OUTPUT ANALYSIS:#####################################

Number of positive predictions (class 1.0) on train set: 5010 out of 9262

Number of positive predictions (class 1.0) on test set: 133 out of 1023

TRAIN METRICS:#####################################

Accuracy: 0.9496, Precision at 83% recall: 0.9706

TEST METRICS:#####################################

Accuracy: 0.8847, Precision at 83% recall: 0.1162

TRIVIAL BASELINE TEST METRICS:#####################################

Test accuracy (only zeros): 0.9619

Test accuracy (only ones): 0.0381

Test accuracy (random): 0.5024, Precision at 83% recall (random) on test: 0.0397

Train the quantum classifiers (also on the training set after angle transform)

We start off by defining a function to train torch models.

[261]:

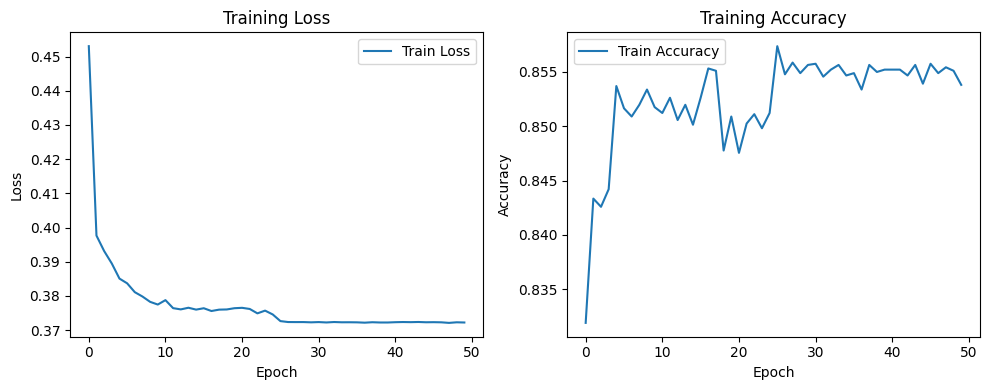

def train_torch_model(model, X_angle, y, n_epochs=50, lr=1e-2, batch_size=64):

optimizer = torch.optim.Adam(model.parameters(), lr=lr)

scheduler = torch.optim.lr_scheduler.StepLR(optimizer, step_size=25, gamma=0.1)

criterion = torch.nn.BCELoss()

dataset = torch.utils.data.TensorDataset(

torch.tensor(X_angle, dtype=torch.float32), torch.tensor(y, dtype=torch.float32)

)

dataloader = torch.utils.data.DataLoader(

dataset, batch_size=batch_size, shuffle=True

)

model.train()

train_losses = []

train_accuracies = []

progress = tqdm(range(n_epochs), desc="Training", leave=False)

for epoch in progress:

epoch_loss = 0.0

epoch_correct = 0

epoch_total = 0

for batch_X, batch_y in dataloader:

optimizer.zero_grad()

outputs = model(batch_X)

loss = criterion(outputs, batch_y)

loss.backward()

optimizer.step()

epoch_loss += loss.item() * batch_X.size(0)

preds = (outputs >= 0.5).float()

epoch_correct += (preds == batch_y).sum().item()

epoch_total += batch_y.size(0)

scheduler.step()

epoch_loss /= len(dataset)

epoch_acc = epoch_correct / epoch_total if epoch_total > 0 else 0.0

train_losses.append(epoch_loss)

train_accuracies.append(epoch_acc)

progress.set_postfix(loss=f"{epoch_loss:.4f}", acc=f"{epoch_acc:.4f}")

if epoch % 10 == 0 or epoch == n_epochs - 1:

print(

f"Epoch {epoch + 1:03d}/{n_epochs} | Train Loss: {epoch_loss:.4f} | Train Acc: {epoch_acc:.4f}"

)

plt.figure(figsize=(10, 4))

plt.subplot(1, 2, 1)

plt.plot(train_losses, label="Train Loss")

plt.xlabel("Epoch")

plt.ylabel("Loss")

plt.title("Training Loss")

plt.legend()

plt.subplot(1, 2, 2)

plt.plot(train_accuracies, label="Train Accuracy")

plt.xlabel("Epoch")

plt.ylabel("Accuracy")

plt.title("Training Accuracy")

plt.legend()

plt.tight_layout()

plt.show()

return {"train_loss": train_losses, "train_accuracy": train_accuracies}

[262]:

# Choose number of quantum classifiers

n_quantum_classifiers = 3

# Initialize quantum classifiers

quantum_classifiers_pca = [QuantumClassifier() for _ in range(n_quantum_classifiers)]

# Select datasets

X_train_pca_quantum = X_train_pca_angle

X_val_pca_quantum = X_val_pca_angle

X_test_pca_quantum = X_test_pca_angle

y_train = np.array(y_train, dtype=np.float32)

y_test = np.array(y_test, dtype=np.float32)

# Train quantum classifiers on PCA dataset

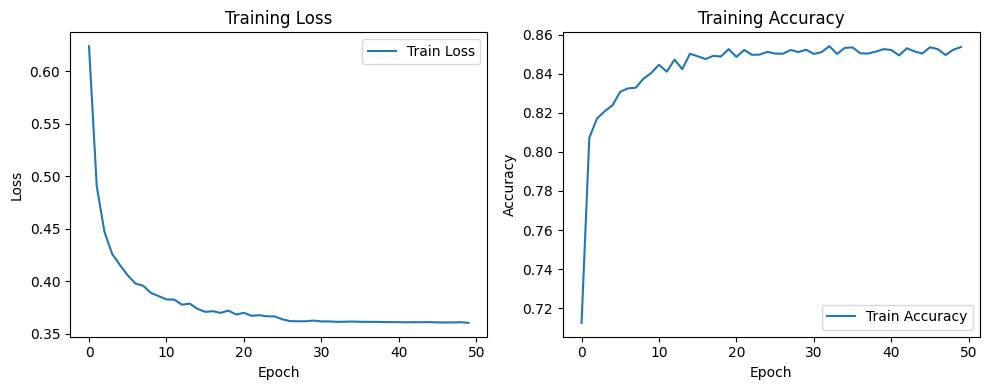

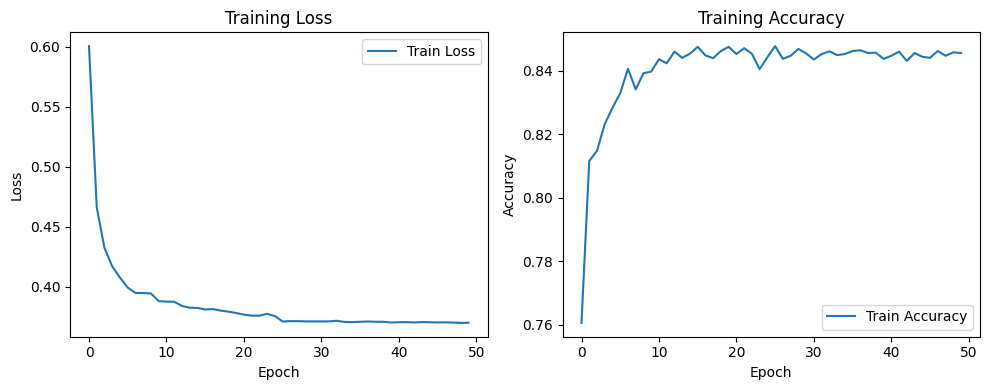

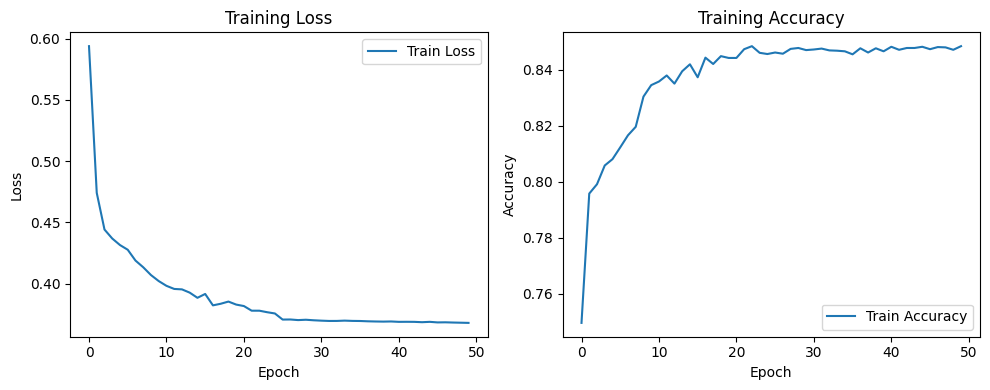

print("Training quantum classifiers on PCA dataset...")

for i, quantum_classifier_pca in enumerate(quantum_classifiers_pca):

train_torch_model(quantum_classifier_pca, X_train_pca_quantum, y_train)

print(f"Trained quantum classifier {i + 1}/{n_quantum_classifiers} on PCA dataset.")

Training quantum classifiers on PCA dataset...

Epoch 001/50 | Train Loss: 0.6240 | Train Acc: 0.7125

Epoch 011/50 | Train Loss: 0.3826 | Train Acc: 0.8446

Epoch 021/50 | Train Loss: 0.3698 | Train Acc: 0.8486

Epoch 031/50 | Train Loss: 0.3616 | Train Acc: 0.8501

Epoch 041/50 | Train Loss: 0.3610 | Train Acc: 0.8522

Epoch 050/50 | Train Loss: 0.3603 | Train Acc: 0.8537

Trained quantum classifier 1/3 on PCA dataset.

Epoch 001/50 | Train Loss: 0.6005 | Train Acc: 0.7606

Epoch 011/50 | Train Loss: 0.3878 | Train Acc: 0.8437

Epoch 021/50 | Train Loss: 0.3769 | Train Acc: 0.8453

Epoch 031/50 | Train Loss: 0.3712 | Train Acc: 0.8436

Epoch 041/50 | Train Loss: 0.3706 | Train Acc: 0.8447

Epoch 050/50 | Train Loss: 0.3701 | Train Acc: 0.8456

Trained quantum classifier 2/3 on PCA dataset.

Epoch 001/50 | Train Loss: 0.5938 | Train Acc: 0.7495

Epoch 011/50 | Train Loss: 0.3983 | Train Acc: 0.8358

Epoch 021/50 | Train Loss: 0.3818 | Train Acc: 0.8442

Epoch 031/50 | Train Loss: 0.3699 | Train Acc: 0.8472

Epoch 041/50 | Train Loss: 0.3689 | Train Acc: 0.8482

Epoch 050/50 | Train Loss: 0.3681 | Train Acc: 0.8484

Trained quantum classifier 3/3 on PCA dataset.

We define a function to print an analysis of a torch model’s output and performance metrics.

[263]:

def torch_model_analysis(torch_model, X_train, y_train, X_test, y_test):

torch_model.eval()

with torch.no_grad():

train_outputs = torch_model(torch.tensor(X_train, dtype=torch.float32)).numpy()

test_outputs = torch_model(torch.tensor(X_test, dtype=torch.float32)).numpy()

print("MODEL OUTPUTS ANALYSIS: ###################################################")

print(

f"Train outputs - min: {train_outputs.min():.4f}, max: {train_outputs.max():.4f}, mean: {train_outputs.mean():.4f}, std: {train_outputs.std():.4f}"

)

print(

f"Number of unique output values on train set of length {len(train_outputs)}: {len(np.unique(train_outputs))}"

)

if len(np.unique(train_outputs)) < 6:

print(

f"Warning: Low number of unique output values; output values all in {np.unique(train_outputs)}"

)

print(

f"Test outputs - min: {test_outputs.min():.4f}, max: {test_outputs.max():.4f}, mean: {test_outputs.mean():.4f}, std: {test_outputs.std():.4f}"

)

print(

f"Number of unique output values on test set of length {len(test_outputs)}: {len(np.unique(test_outputs))}"

)

if len(np.unique(test_outputs)) < 6:

print(

f"Warning: Low number of unique output values; output values all in {np.unique(test_outputs)}"

)

train_predictions = (train_outputs >= 0.5).astype(float)

test_predictions = (test_outputs >= 0.5).astype(float)

train_accuracy = np.mean(train_predictions == y_train)

test_accuracy = np.mean(test_predictions == y_test)

train_precision = precision_at_fixed_recall(

y_train, train_outputs, target_recall=0.83

)

test_precision = precision_at_fixed_recall(y_test, test_outputs, target_recall=0.83)

print(

"\nMODEL PERFORMANCE ANALYSIS: ###################################################"

)

print(

f"Training accuracy: {train_accuracy:.4f}, Precision at 83% recall: {train_precision:.4f}"

)

print(

f"Test accuracy: {test_accuracy:.4f}, Precision at 83% recall: {test_precision:.4f}"

)

only_zero = np.array([0.0] * len(y_test))

only_one = np.array([1.0] * len(y_test))

random_outputs = np.random.rand(len(y_test))

random_preds = (random_outputs >= 0.5).astype(float)

accuracy_only_zero = np.mean(only_zero == y_test)

accuracy_only_one = np.mean(only_one == y_test)

accuracy_random = np.mean(random_preds == y_test)

precision_random = precision_at_fixed_recall(

y_test, random_outputs, target_recall=0.83

)

print(

f"\nTRIVIAL PREDICTORS TEST PERFORMANCE: ###################################################"

)

print(f"Only zero predictor - Test accuracy: {accuracy_only_zero:.4f}")

print(f"Only one predictor - Test accuracy: {accuracy_only_one:.4f}")

print(

f"Random predictor - Test accuracy: {accuracy_random:.4f}, Precision at 83% recall (on test): {precision_random:.4f}"

)

5.2 First Quantum Classifier Output And Performance Analysis (Train And Validation)

[264]:

torch_model_analysis(

quantum_classifiers_pca[0], X_train_pca_quantum, y_train, X_val_pca_quantum, y_val

)

MODEL OUTPUTS ANALYSIS: ###################################################

Train outputs - min: 0.0061, max: 0.9917, mean: 0.5024, std: 0.3591

Number of unique output values on train set of length 9262: 4773

Test outputs - min: 0.0072, max: 0.9904, mean: 0.2637, std: 0.2732

Number of unique output values on test set of length 1023: 1023

MODEL PERFORMANCE ANALYSIS: ###################################################

Training accuracy: 0.8538, Precision at 83% recall: 0.8705

Test accuracy: 0.8221, Precision at 83% recall: 0.2481

TRIVIAL PREDICTORS TEST PERFORMANCE: ###################################################

Only zero predictor - Test accuracy: 0.9619

Only one predictor - Test accuracy: 0.0381

Random predictor - Test accuracy: 0.4966, Precision at 83% recall (on test): 0.0418

5.3 Train The NN Baseline

[265]:

train_pca_nn = X_train_pca

val_pca_nn = X_val_pca

test_pca_nn = X_test_pca

nn_pca = NeuralNetWork(n_features=train_pca_nn.shape[1], hidden_size=4)

print("Number of parameters in NN:", sum(p.numel() for p in nn_pca.parameters()))

train_torch_model(nn_pca, train_pca_nn, y_train)

print("Training of NN baseline completed on PCA dataset.")

Number of parameters in NN: 29

Epoch 001/50 | Train Loss: 0.4530 | Train Acc: 0.8319

Epoch 011/50 | Train Loss: 0.3788 | Train Acc: 0.8512

Epoch 021/50 | Train Loss: 0.3765 | Train Acc: 0.8475

Epoch 031/50 | Train Loss: 0.3724 | Train Acc: 0.8558

Epoch 041/50 | Train Loss: 0.3723 | Train Acc: 0.8552

Epoch 050/50 | Train Loss: 0.3722 | Train Acc: 0.8538

Training of NN baseline completed on PCA dataset.

5.4 Analysis Of NN Baseline Outputs And Performance Metrics

[266]:

torch_model_analysis(nn_pca, train_pca_nn, y_train, val_pca_nn, y_val)

MODEL OUTPUTS ANALYSIS: ###################################################

Train outputs - min: 0.0000, max: 1.0000, mean: 0.4999, std: 0.3691

Number of unique output values on train set of length 9262: 4773

Test outputs - min: 0.0000, max: 1.0000, mean: 0.2602, std: 0.2874

Number of unique output values on test set of length 1023: 1023

MODEL PERFORMANCE ANALYSIS: ###################################################

Training accuracy: 0.8540, Precision at 83% recall: 0.8579

Test accuracy: 0.8094, Precision at 83% recall: 0.2171

TRIVIAL PREDICTORS TEST PERFORMANCE: ###################################################

Only zero predictor - Test accuracy: 0.9619

Only one predictor - Test accuracy: 0.0381

Random predictor - Test accuracy: 0.5054, Precision at 83% recall (on test): 0.0438

5.5 Training Of KNN Performance And Analysis Of Performance Metrics

[267]:

# Training KNN on PCA dataset

knn_pca.fit(X_train_pca, y_train)

# Analyze KNN predictions on PCA dataset

sklearn_model_analysis(knn_pca, X_train_pca, y_train, X_test_pca, y_test)

MODEL OUTPUT ANALYSIS:#####################################

Number of positive predictions (class 1.0) on train set: 4834 out of 9262

Number of positive predictions (class 1.0) on test set: 77 out of 1023

TRAIN METRICS:#####################################

Accuracy: 0.9781, Precision at 83% recall: 1.0000

TEST METRICS:#####################################

Accuracy: 0.9159, Precision at 83% recall: 0.0381

TRIVIAL BASELINE TEST METRICS:#####################################

Test accuracy (only zeros): 0.9619

Test accuracy (only ones): 0.0381

Test accuracy (random): 0.4917, Precision at 83% recall (random) on test: 0.0389

5.6 Training of the hybrid model

Now that all subsidiary models have been trained, we can optimize the complete QuantumEnhancedAdaBoost

Train complete QuantumEnhancedAdaBoost model (on training set)

[268]:

quantum_enhanced_adaboost_pca = QuantumEnhancedAdaBoost(

classical_model=adaboost_pca, quantum_estimators=quantum_classifiers_pca

)

precision_before = precision_at_fixed_recall(

y_val,

quantum_enhanced_adaboost_pca.predict_proba(X_val_pca, X_val_pca_angle),

target_recall=0.83,

)

print(

f"Precision at 83% recall for QuantumEnhancedAdaBoost on PCA validation dataset before weight optimization: {precision_before:.4f}"

)

print(

"Optimizing ensemble weights for QuantumEnhancedAdaBoost on PCA validation dataset..."

)

print(

f"Initial ensemble weights for QuantumEnhancedAdaBoost on PCA validation dataset: {quantum_enhanced_adaboost_pca.weights}"

)

quantum_enhanced_adaboost_pca.fit(X_val_pca, X_val_pca_angle, y_val)

print(

f"Optimal ensemble weights for QuantumEnhancedAdaBoost on PCA validation dataset: {quantum_enhanced_adaboost_pca.weights}"

)

precision_after = precision_at_fixed_recall(

y_val,

quantum_enhanced_adaboost_pca.predict_proba(X_val_pca, X_val_pca_angle),

target_recall=0.83,

)

print(

f"Precision at 83% recall for QuantumEnhancedAdaBoost on PCA validation dataset after weight optimization: {precision_after:.4f}\n"

)

Precision at 83% recall for QuantumEnhancedAdaBoost on PCA validation dataset before weight optimization: 0.2973

Optimizing ensemble weights for QuantumEnhancedAdaBoost on PCA validation dataset...

Initial ensemble weights for QuantumEnhancedAdaBoost on PCA validation dataset: [0.25 0.25 0.25 0.25]

Optimal ensemble weights for QuantumEnhancedAdaBoost on PCA validation dataset: [0.0625 0.06320711 0.81179289 0.0625 ]

Precision at 83% recall for QuantumEnhancedAdaBoost on PCA validation dataset after weight optimization: 0.3084

6. Evaluation (Test Set)

For evaluation, we will consider two metrics: accuracy and precision at 83% recall on the test set.

Evaluation of classical baseline

[269]:

test_predictions_pca_adaboost = adaboost_pca.predict(X_test_pca)

adaboost_accuracy_pca = (test_predictions_pca_adaboost == y_test).mean()

adaboost_precision_pca = precision_at_fixed_recall(

y_test, adaboost_pca.predict_proba(X_test_pca), target_recall=0.83

)

results = pd.DataFrame(

{

"PCA": [adaboost_accuracy_pca, adaboost_precision_pca],

},

index=["Accuracy", "Precision @ Recall=0.83"],

)

results

[269]:

| PCA | |

|---|---|

| Accuracy | 0.891496 |

| Precision @ Recall=0.83 | 0.157895 |

[270]:

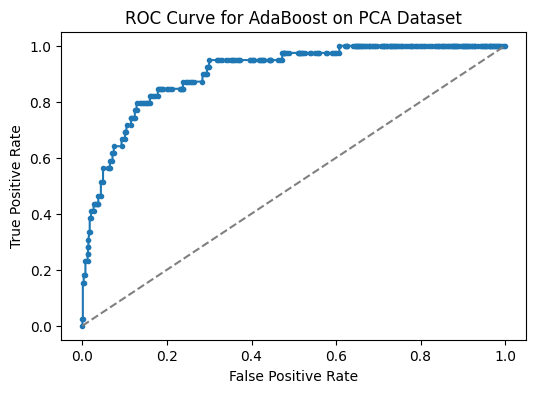

probas = adaboost_pca.predict_proba(X_test_pca)

fpr, tpr, thresholds = roc_curve(y_test, probas)

plt.figure(figsize=(6, 4))

plt.plot(fpr, tpr, marker=".")

plt.plot(

[0, 1], [0, 1], linestyle="--", color="gray"

) # Add diagonal line for reference

plt.xlabel("False Positive Rate")

plt.ylabel("True Positive Rate")

plt.title("ROC Curve for AdaBoost on PCA Dataset")

plt.show()

print(f"AUC: {auc(fpr, tpr):.4f}")

AUC: 0.9028

6.1 Evaluation Of The QuantumEnhancedAdaBoost

[271]:

test_predictions_pca_hybrid = quantum_enhanced_adaboost_pca.predict(

X_test_pca, X_test_pca_angle

)

hybrid_accuracy_pca = (test_predictions_pca_hybrid == y_test).mean()

hybrid_precision_pca = precision_at_fixed_recall(

y_test,

quantum_enhanced_adaboost_pca.predict_proba(X_test_pca, X_test_pca_angle),

target_recall=0.83,

)

results_hybrid = pd.DataFrame(

{

"PCA": [hybrid_accuracy_pca, hybrid_precision_pca],

},

index=["Accuracy", "Precision @ Recall=0.83"],

)

results_hybrid

[271]:

| PCA | |

|---|---|

| Accuracy | 0.847507 |

| Precision @ Recall=0.83 | 0.186441 |

[272]:

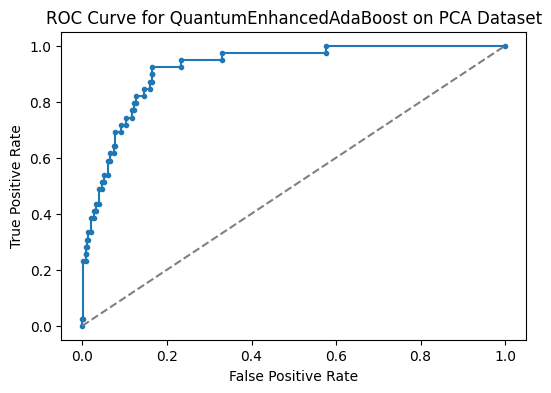

probas = quantum_enhanced_adaboost_pca.predict_proba(X_test_pca, X_test_pca_angle)

fpr, tpr, thresholds = roc_curve(y_test, probas)

plt.figure(figsize=(6, 4))

plt.plot(fpr, tpr, marker=".")

plt.plot(

[0, 1], [0, 1], linestyle="--", color="gray"

) # Add diagonal line for reference

plt.xlabel("False Positive Rate")

plt.ylabel("True Positive Rate")

plt.title("ROC Curve for QuantumEnhancedAdaBoost on PCA Dataset")

plt.show()

print(f"AUC: {auc(fpr, tpr):.4f}")

AUC: 0.9209

6.2 Final Look At Our Models

[273]:

num_positives_pca = (test_predictions_pca_adaboost == 1.0).sum()

print(

f"Number of samples predicted as positive (bankrupt) by the PCA AdaBoost model: {num_positives_pca}"

)

num_positives_pca = (test_predictions_pca_hybrid == 1.0).sum()

print(

f"Number of samples predicted as positive (bankrupt) by the PCA hybrid model: {num_positives_pca}"

)

print(f"Total number of positive samples in test set: {(y_test == 1.0).sum()}")

total_samples = len(y_test)

print(f"Total number of samples in test set: {total_samples}")

Number of samples predicted as positive (bankrupt) by the PCA AdaBoost model: 126

Number of samples predicted as positive (bankrupt) by the PCA hybrid model: 183

Total number of positive samples in test set: 39

Total number of samples in test set: 1023

7 Conclusion

We have seen, through the hybrid model’s weights, that this model indeed gives more importance to submodels that reach high precision at 83% recall on the validation set. We see now how this reflects on the test set; a lower accuracy and a tendency to over-predict the positive class, but a higher precision at 83% recall and a higher Area Under the Curve (AUC).

We can now justify the use of a QuantumEnhancedAdaBoost optimized on the precision for a given recall based on which metric is most important for a given task. We have also seen how oversampling can help in imbalanced dataset settings.